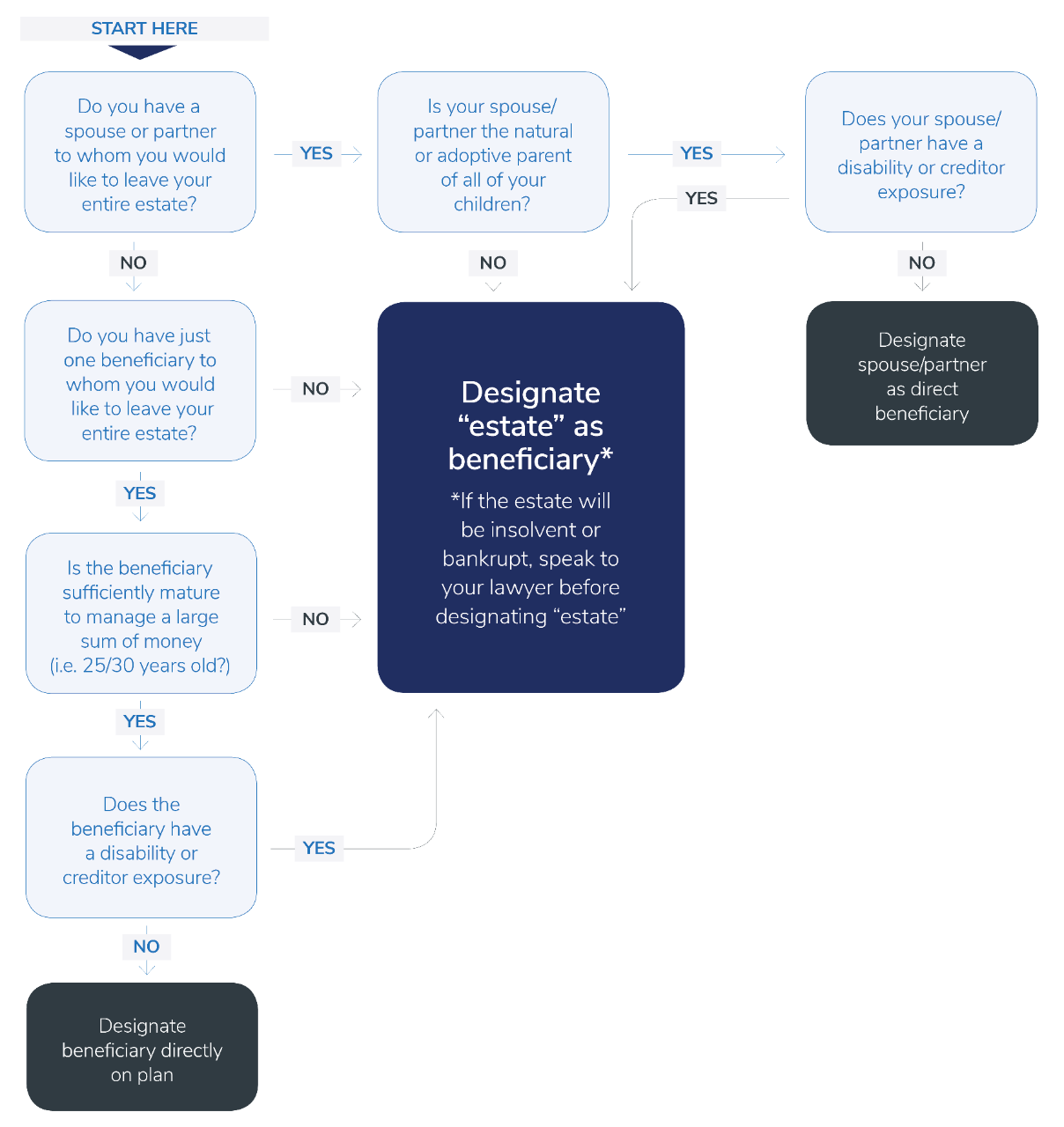

Many Canadians designate a direct beneficiary on their RRSP, RRIF, TFSA or insurance policies without giving it a second thought (although in Quebec, beneficiary designations are only effective on insurance policies). However, designating a direct beneficiary is not recommended for many plan/policy owners, where they have non-traditional or unique family situations, as it can lead to unfavourable tax implications for beneficiaries. We’ve created a beneficiary designations decision tree to help you understand the factors you should consider in designating a plan/policy beneficiary.

Generally, direct beneficiary designations are most appropriate in the following circumstances:

- When you’re in a first marriage or relationship and want to leave your entire estate to your surviving spouse/partner.

- When you will not be survived by a spouse/partner, and you want to leave your entire estate to only one beneficiary (e.g., an only child or just one charity); or

- Where there is a concern that your estate may be bankrupt or insolvent (and you want assets to pass outside of your estate to avoid exposure to estate creditors).

However, designating direct beneficiaries is usually not that straightforward. There are other important factors to consider, and designating a direct beneficiary is strongly discouraged in these situations:

- Where any of your beneficiaries is a minor (or young adult)

- Where your beneficiary is person with a disability

- When you are part of a blended families (i.e., you are in a relationship where your spouse or partner is not the natural or adoptive parent of all of your children)

- Where there are multiple beneficiaries (e.g., you have more than one child)

- Where there are secondary, alternate or contingent designations; or

- In situations where a beneficiary has creditor exposure (e.g., a business owner)